SBIR Uncertainty and Funding Alternatives

February 19, 2026 | Becky Nictakis

For more than forty years, the Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) programs have served as an on-ramp for small businesses into the defense innovation ecosystem. SBIR funding from the Department of War (DOW), previously the Department of Defense (DOD), has enabled early-stage research, supported risk reduction, and introduced thousands of small firms to defense customers—many of whom later transitioned technologies into programs of record.

Today, however, the future of SBIR is uncertain. Questions about program design, the concentration of awards among repeat winners, and the ongoing uncertainty surrounding reauthorization have created a more complex environment for companies pursuing DOW funding. As a result, defense innovators must look beyond SBIR alone and adopt a more diversified engagement strategy.

One of the most persistent critiques of SBIR within the defense community is the perception that large primes, or small firms closely aligned with them, “mill” SBIRs as a recurring funding source rather than as a pathway to commercialized capability. A relatively small number of companies have won a disproportionate share of awards over time, raising concerns among policymakers that SBIR dollars are being recycled among a handful of companies instead of expanding the defense industrial base.

At the same time, DOW stakeholders acknowledge that repeat awardees often succeed precisely because they understand military requirements, compliance, and transition pathways. From the military’s perspective, reliability, technical maturity, and the ability to deliver under government constraints matter as much as novelty. The tension is not simply about who wins SBIRs, but whether SBIR outcomes are translating into operational impact, acquisition interest, or sustained commercialization.

This debate has intensified as the DOW increasingly emphasizes speed, transition, and relevance to near-term mission needs, priorities that do not always align with the traditional, phased SBIR model.

Reauthorization Uncertainty and Its Implications

Compounding these structural concerns is the unresolved status of SBIR/STTR reauthorization. As of 2026, the statutory authority for both programs has lapsed, halting new solicitations and delaying awards pending congressional action. While multiple legislative proposals remain under discussion, including bills that would modernize the program, impose performance benchmarks, or even make SBIR permanent, no consensus has yet emerged.

For defense contractors and technology firms, this uncertainty creates real risk. SBIR timelines were already long by commercial standards and the added unpredictability of reauthorization makes it difficult to plan hiring, product development, and capital strategy around SBIR alone. For companies targeting DOW customers in particular, reliance on SBIR as the primary entry point is increasingly misaligned with how the Army is buying and experimenting today.

Defense Funding Alternatives

In this environment, companies should view SBIR as one tool among many—not the sole gateway to Army funding or relationships. Several alternative mechanisms now offer faster, more flexible paths for engagement, especially for firms with marketable dual-use products or mature prototypes.

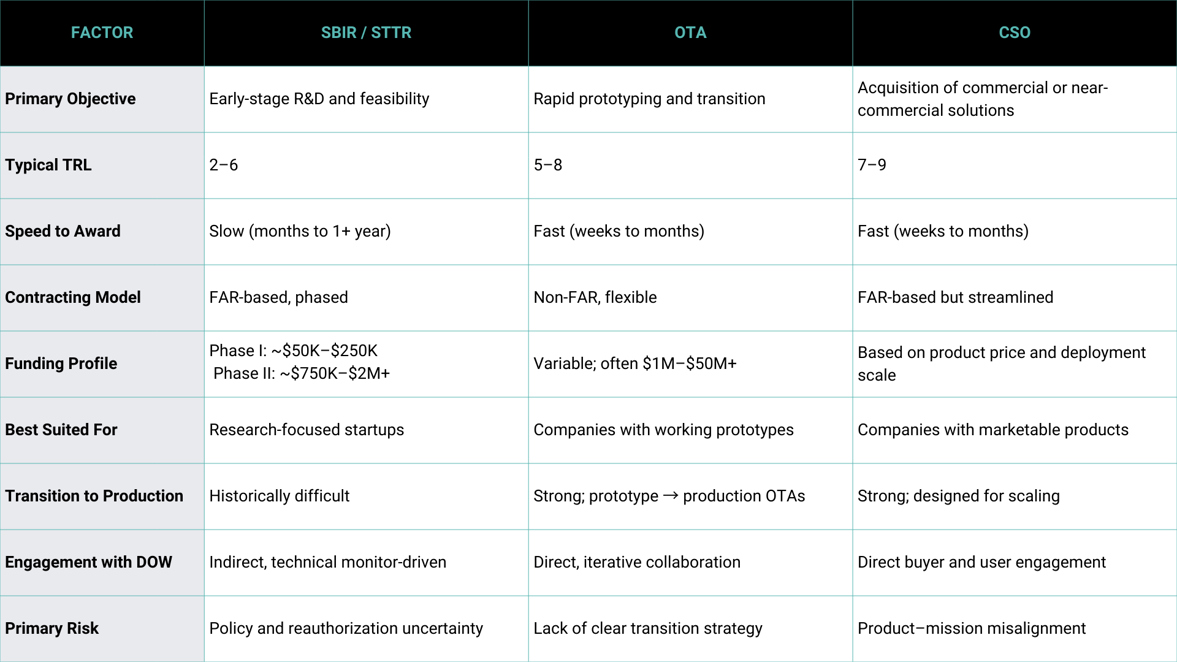

1. Other Transaction Authorities (OTAs)

OTAs have become a cornerstone of Army innovation strategy. They allow the government to prototype, test, and iterate technologies outside the constraints of the Federal Acquisition Regulation (FAR). For companies with demonstrated capabilities, OTAs offer several advantages:

-

-

Faster award timelines and simplified contracting

-

Direct engagement with program offices and end users

-

Clearer pathways from prototype to production OTAs

-

For firms seeking to develop long-term relationships with DOW, OTAs are often more effective than SBIRs because they focus on solving defined operational problems rather than funding exploratory research. Participation in Army consortia and alignment with trusted OTA intermediaries can significantly increase access to these opportunities.

2. Commercial Solutions Openings (CSOs)

CSOs are particularly attractive for companies with existing products that can be adapted for military use. Unlike SBIRs, CSOs are designed to identify and scale commercially proven technologies that address defense needs. For DOW customers, CSOs reduce risk by leveraging market-validated solutions; for companies, they shorten the path to revenue and adoption.

CSOs also serve as a relationship-building mechanism. Successful engagements often lead to follow-on contracts, pilot deployments, or integration into larger DOW programs—outcomes that are harder to achieve through SBIR alone.

3. Broad Agency Announcements and Targeted R&D Programs

BAAs, Army Applied Research solicitations, and DARPA programs remain viable options for companies pursuing advanced or mission-specific research. While competitive, these mechanisms can support higher funding levels and deeper collaboration with government technical teams.

Whether SBIR is reauthorized with reforms or restored largely intact, it is clear that the DOW is prioritizing speed, transition, and deployable capability. Companies that base their strategy solely on SBIR risk being out of step with how DOW is engaging industry today.

The most resilient defense innovators are those who understand SBIR as an entry point and who actively pursue OTAs, CSOs, and other flexible contracting pathways to demonstrate value, build trust, and move technologies into the hands of soldiers. In a crowded and uncertain funding environment, strategic agility is the key to success.

At-a-Glance Comparison

Address

500 North Capitol Street NW

Suite 210

Washington, DC 20001